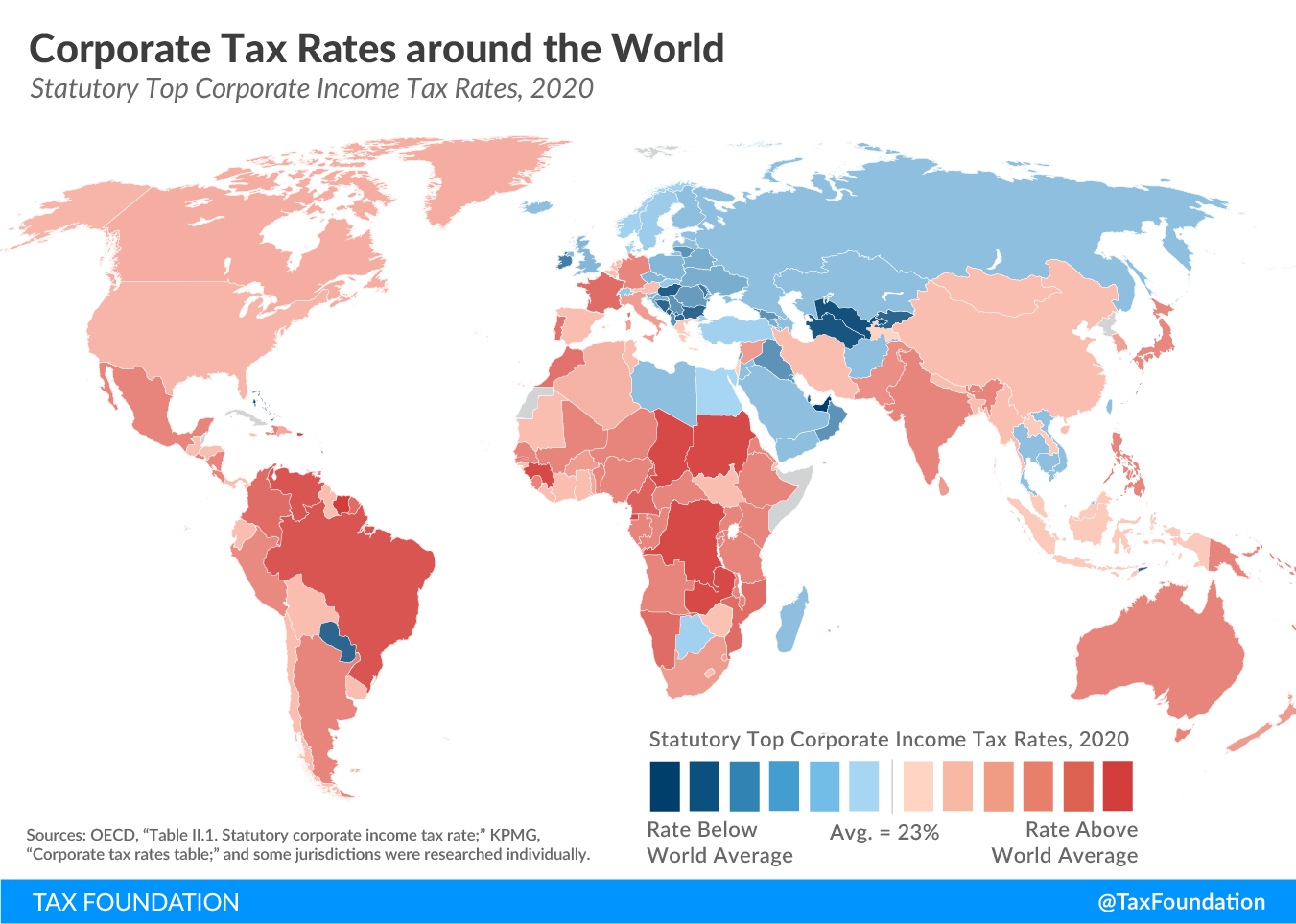

Corporate tax rates have been a contentious issue in American politics, especially following the implications of the Tax Cuts and Jobs Act of 2017. This legislation drastically lowered corporate taxes from 35% to 21%, igniting a debate on its impact on corporate tax revenue and economic growth. Harvard economist Gabriel Chodorow-Reich, in his latest analysis, scrutinizes the real-world outcomes of this significant tax reform and its subsequent effect on business investments and wages. He argues that despite initial claims that tax cuts would spur growth, the actual data suggests a more complex relationship between corporate taxation and economic performance. As Congress gears up for another tax battle in 2025, understanding the nuances of corporate tax policy and the effects of prior tax cuts will be crucial for future discussions.

The discussion surrounding business taxation in the U.S. has evolved significantly, particularly with the ongoing evaluations of past reforms. The reduction in business tax obligations, notably seen in the Tax Reform Act of 2017, has prompted economists to explore the implications of such fiscal policies on the economy at large. Gabriel Chodorow-Reich’s recent research sheds light on how these adjustments in corporate tax rates have influenced areas like corporate investment and income distribution. With debates intensifying over whether to raise or maintain these tax levels, it becomes imperative to dissect the relationship between corporate taxes and overall economic stability. Thus, this examination of corporate taxation remains central to understanding the shifting landscape of economic policy and its impact on taxpayers.

The Impact of the 2017 Tax Cuts and Jobs Act on Corporate Tax Rates

The 2017 Tax Cuts and Jobs Act (TCJA) dramatically altered the landscape of corporate taxation in the United States, slashing the corporate tax rate from 35% to 21%. This profound shift was intended to stimulate economic growth by encouraging business investment and expansion. However, the actual impact of these changes has become a point of contention among economists and policymakers alike. Research conducted by experts like Gabriel Chodorow-Reich has revealed that while capital investments did see a modest increase of about 11%, these financial gains were dwarfed by the immediate decline in corporate tax revenue, which plummeted by nearly 40% following the law’s implementation.

Chodorow-Reich’s analysis further highlights that although the TCJA led to significant corporate profit growth in subsequent years, it was not without its drawbacks. The initial reduction in corporate tax revenue was staggering, with estimates suggesting losses upwards of $100 billion annually for the federal government. This situation underscores a critical debate about the effectiveness of tax cuts; proponents argue that tax reductions catalyze economic expansion and investment, while critics like Chodorow-Reich stress the importance of a balanced tax strategy that takes into account fiscal sustainability.

Frequently Asked Questions

What impact did the 2017 Tax Cuts and Jobs Act have on corporate tax rates?

The 2017 Tax Cuts and Jobs Act (TCJA) significantly reduced the corporate tax rate from 35% to 21%, aiming to stimulate economic growth and investment. However, studies, including one by Gabriel Chodorow-Reich, indicate that the tax cuts did not generate sufficient revenue increases to offset the loss in corporate tax revenue, which dropped significantly following the reduction.

How did corporate tax cuts affect corporate tax revenue?

Following the implementation of the TCJA, corporate tax revenue initially plummeted by 40%. Although it eventually rebounded, researchers like Gabriel Chodorow-Reich emphasize that this resurgence was due to unexpected business profits rather than a direct result of the tax cuts stimulating investment as initially hoped.

Did the reductions in corporate tax rates lead to increased business investments?

Yes, the TCJA did correlate with a rise in business investments, which increased by about 11%. However, Gabriel Chodorow-Reich’s research suggests that targeted provisions like immediate expensing of capital investments were more effective in driving growth than the broad statutory rate cuts.

What are the arguments for raising corporate tax rates in light of the TCJA?

Proponents of raising corporate tax rates argue that the dramatic cuts under the TCJA resulted in substantial revenue losses without proportionate benefits for workers or the economy. Gabriel Chodorow-Reich supports the idea that while tax rates influence corporate behavior, restoring higher statutory rates combined with effective investment incentives could lead to better economic outcomes.

What did Gabriel Chodorow-Reich conclude about corporate tax policy and its effects?

Gabriel Chodorow-Reich concluded that corporate tax policy directly influences investment decisions by firms. Nevertheless, the empirical evidence from the post-TCJA environment suggests that the anticipated wage increases and economic benefits have not materialized to the extent claimed by proponents of the tax cuts.

How might future corporate tax policy reform be approached?

Future reforms might involve a balanced approach that raises corporate tax rates while simultaneously reinstating targeted provisions like expensing to stimulate investment. This dual strategy could potentially enhance tax revenues while promoting economic growth, as highlighted by Gabriel Chodorow-Reich’s findings.

| Key Point | Details |

|---|---|

| Corporate Tax Rate Changes | The TCJA permanently reduced the corporate tax rate from 35% to 21%. |

| Effects on Revenue | The law is projected to reduce federal corporate tax revenue by $100-150 billion per year. |

| Investment Impacts | Corporate investment increased by about 11% after TCJA implementation, driven by specific provisions. |

| Wage Growth | Wage increases post-TCJA were around $750 per employee annually, much lower than anticipated. |

| Political Debate | Corporate tax rates are a key issue in the upcoming elections, with both parties proposing differing strategies. |

| Economic Context | The TCJA took place after 30 years without major tax reform, amidst global economic changes. |

Summary

Corporate Tax Rates are a significant topic in the current political landscape, as Congress prepares for a heated tax battle in 2025. Recent analyses reveal mixed outcomes from the Tax Cuts and Jobs Act of 2017, indicating that while corporate tax rates were cut substantially, the expected benefits for revenue and wage growth did not materialize as anticipated. This raises important questions about the effectiveness of such tax policies in fostering economic growth.